January brought a noticeable increase in market volatility, largely driven by geopolitical headlines involving tariffs and the Trump administration’s comments regarding Greenland. Despite the noise, the S&P 500 managed a 1.45% positive return, extending its three-year winning streak. Over at the Federal Reserve, interest rates were held steady during their January meeting, while Kevin Warsh—President Trump’s nominee to replace Jerome Powell as Fed Chairman—began gathering support for his confirmation.

Moving into early February, artificial intelligence (AI) took center stage. Software-as-a-service (SaaS) companies—the kind that power much of our modern medical and corporate infrastructure—saw their stocks take a hit. Investors worried that businesses might replace monthly software subscriptions with powerful, customizable AI tools built in-house. While many analysts feel predicting a “SaaS-pocalypse” is premature, investors quickly rotated their funds out of the technology sector and into materials, industrials, and financial stocks. Add in a late but surprisingly positive January labor report, and unexpected tariff announcements following a Supreme Court ruling, and it’s clear why markets have felt turbulent.

Let’s get into the data:

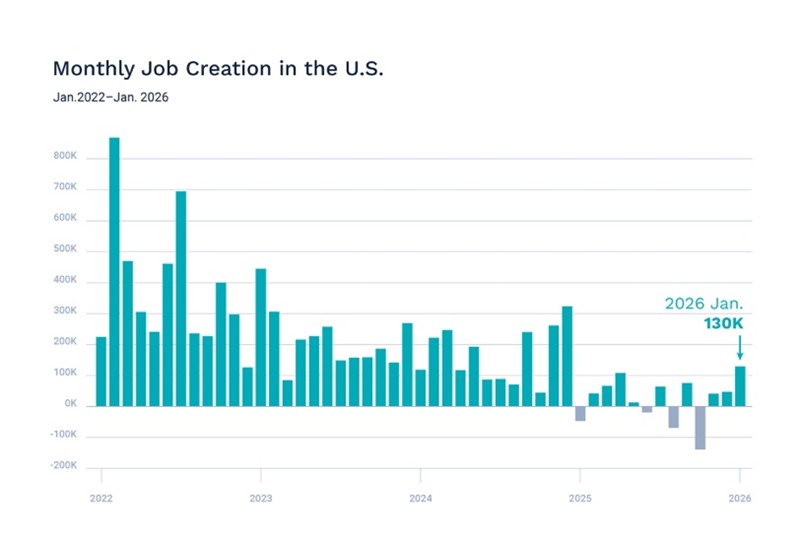

- Job Growth Surged: Non-farm payrolls added 130,000 jobs in January, more than double the 55,000 expected, pushing the unemployment rate down to 4.3%.

- Inflation Cooled: The Consumer Price Index grew by 2.4% over the last twelve months, which is a 0.3 percentage point drop from December and the lowest reading we have seen since May 2025.

- Consumer Sentiment Improved Slightly: The University of Michigan Consumer Sentiment Index ticked up to 56.6 from 56.4. However, this recovery remains “K-shaped,” meaning wealthier households are feeling more optimistic while lower-income groups are experiencing declining sentiment.

- Economic Growth Slowed: Fourth-quarter GDP grew at an annualized rate of just 1.4%, which missed the estimated 2.5% gain.

What Does the Data Add Up To?

On the surface, a combination of a weaker broader economy and a strong labor market might push the Federal Reserve to restart interest rate cuts. However, Federal Reserve Governor Waller cautioned in a February 23rd speech that a single month of strong job growth does not make a trend, especially since 2025 was the weakest year for job creation in a non-recession year since 2002. He also noted that last year’s government shutdown likely reduced fourth-quarter GDP by a full percentage point, which should theoretically boost the first quarter of 2026 by that same amount. When smoothing out those anomalies, he expects GDP to hover above 2%. With Chairman Powell’s term ending in May, it is highly possible that rate changes will be paused until a new Chairman takes over at the June meeting.

In trade news, the Supreme Court struck down tariffs that had been imposed under the International Emergency Powers Act. While the President quickly announced new tariffs in response, research from The Budget Lab at Yale suggests the effective tariff rate will actually be lower. This development could reduce costs for U.S. households and help stabilize inflation.

Chart of the Month: Labor Surprises on the Upside

A strong highlight for our medical professional clients: the healthcare sector led January’s job growth, adding 82,000 positions. This robust labor market, contrasted with weaker GDP, leaves the door open for the Fed to consider lowering rates in the future.

Source: Bureau of Labor Statistics; Axios Visuals

Equity Markets in January

- The S&P 500 gained 1.44% for the month, which is also its year-to-date return.

- The Dow Jones Industrial Average rose 1.80% in January, starting the year on a stronger note than its December finish.

- The S&P MidCap 400 climbed 4.05% for the month, significantly outpacing the large-cap indices.

- The S&P SmallCap 600 was the standout performer, surging 5.39% in January as investors moved into smaller-capitalization equities.

This positive “January barometer” is historically an encouraging sign; over the past 40 years, there have been 25 years with a positive January. In 84% of those years, the market finished the full year in positive territory. Additionally, investor confidence is rising: The Charles Schwab Trading Activity Index (STAX) increased to 49.96 in January from December’s 48.48. Notably, Gen X investors—which encompasses many of you reading this—were the most active buyers during the month.

Bond Markets in January

The 10-year U.S. Treasury ended the month at a yield of 4.24%, up from 4.17% the prior month. The 30-year U.S. Treasury ended January at 4.84%, up from 4.80%. The Bloomberg U.S. Aggregate Bond Index returned 0.11% in January. The Bloomberg Municipal Bond Index returned 0.94% for the month.

The Smart Investor

The new year has kicked off at a sprint, bringing with it headline-driven volatility. With AI disruption becoming the newest market narrative, it is easy to get distracted. What should you focus on instead? Yourself, your family’s goals, and your long-term plan.

Building a financial framework that can weather market shocks while remaining flexible enough to capture new opportunities relies heavily on proper asset allocation. Whether you are a VP navigating stock options or a surgeon balancing practice revenues with kids approaching high school, understanding your risk tolerance and your specific financial needs is what keeps your plan successfully on track.

As we move further into the year, it is a great time to dive a little deeper. Do you understand your own “money story?” What really drives your financial decisions, and what are your fears? Tactical saving and investing are only part of the equation. We are always available for a discussion to keep your financial journey moving forward smoothly.

February Market Commentary – Labor, Tariffs, AI and Rates

February Market Commentary – Labor, Tariffs, AI and Rates

January brought a noticeable increase in market volatility, largely driven by geopolitical headlines involving tariffs and the Trump administration’s comments regarding Greenland. Despite the noise, the S&P 500 managed a 1.45% positive return, extending its three-year winning streak. Over at the Federal Reserve, interest rates were held steady during their January meeting, while Kevin Warsh—President Trump’s nominee to replace Jerome Powell as Fed Chairman—began gathering support for his confirmation.

Moving into early February, artificial intelligence (AI) took center stage. Software-as-a-service (SaaS) companies—the kind that power much of our modern medical and corporate infrastructure—saw their stocks take a hit. Investors worried that businesses might replace monthly software subscriptions with powerful, customizable AI tools built in-house. While many analysts feel predicting a “SaaS-pocalypse” is premature, investors quickly rotated their funds out of the technology sector and into materials, industrials, and financial stocks. Add in a late but surprisingly positive January labor report, and unexpected tariff announcements following a Supreme Court ruling, and it’s clear why markets have felt turbulent.

Let’s get into the data:

What Does the Data Add Up To?

On the surface, a combination of a weaker broader economy and a strong labor market might push the Federal Reserve to restart interest rate cuts. However, Federal Reserve Governor Waller cautioned in a February 23rd speech that a single month of strong job growth does not make a trend, especially since 2025 was the weakest year for job creation in a non-recession year since 2002. He also noted that last year’s government shutdown likely reduced fourth-quarter GDP by a full percentage point, which should theoretically boost the first quarter of 2026 by that same amount. When smoothing out those anomalies, he expects GDP to hover above 2%. With Chairman Powell’s term ending in May, it is highly possible that rate changes will be paused until a new Chairman takes over at the June meeting.

In trade news, the Supreme Court struck down tariffs that had been imposed under the International Emergency Powers Act. While the President quickly announced new tariffs in response, research from The Budget Lab at Yale suggests the effective tariff rate will actually be lower. This development could reduce costs for U.S. households and help stabilize inflation.

Chart of the Month: Labor Surprises on the Upside

A strong highlight for our medical professional clients: the healthcare sector led January’s job growth, adding 82,000 positions. This robust labor market, contrasted with weaker GDP, leaves the door open for the Fed to consider lowering rates in the future.

Source: Bureau of Labor Statistics; Axios Visuals

Equity Markets in January

This positive “January barometer” is historically an encouraging sign; over the past 40 years, there have been 25 years with a positive January. In 84% of those years, the market finished the full year in positive territory. Additionally, investor confidence is rising: The Charles Schwab Trading Activity Index (STAX) increased to 49.96 in January from December’s 48.48. Notably, Gen X investors—which encompasses many of you reading this—were the most active buyers during the month.

Bond Markets in January

The 10-year U.S. Treasury ended the month at a yield of 4.24%, up from 4.17% the prior month. The 30-year U.S. Treasury ended January at 4.84%, up from 4.80%. The Bloomberg U.S. Aggregate Bond Index returned 0.11% in January. The Bloomberg Municipal Bond Index returned 0.94% for the month.

The Smart Investor

The new year has kicked off at a sprint, bringing with it headline-driven volatility. With AI disruption becoming the newest market narrative, it is easy to get distracted. What should you focus on instead? Yourself, your family’s goals, and your long-term plan.

Building a financial framework that can weather market shocks while remaining flexible enough to capture new opportunities relies heavily on proper asset allocation. Whether you are a VP navigating stock options or a surgeon balancing practice revenues with kids approaching high school, understanding your risk tolerance and your specific financial needs is what keeps your plan successfully on track.

As we move further into the year, it is a great time to dive a little deeper. Do you understand your own “money story?” What really drives your financial decisions, and what are your fears? Tactical saving and investing are only part of the equation. We are always available for a discussion to keep your financial journey moving forward smoothly.

RECENT ARTICLES

Health Savings Accounts Just Got More Powerful

Getting to a Closing in a Red-Hot Real Estate Market

Turning Your Side Hustle into a Full-Time Gig

Understanding Alternative Investments

The Pre-IPO Checklist for Employees