September Recap and October Outlook

September equity markets ended the month in positive territory, but with volatility increased. The VIX, the markets “fear index” closed higher than last month, at 16.73, up from 15.00. Intramonth, the values ranged from a high of 23.76 and a low of 14.90.

September’s somewhat surprisingly 50-basis point reduction in interest rates kicked of the regime change in monetary policy with a big move downwards. Subsequent data releases, including a particularly strong September non-farm payrolls number, may put a damper on expectations going forward, but the long-awaited loosening cycle is finally here. However, with an election looming and heightened tension in the middle east volatility will continue to affect markets and investor behavior alike.

Let’s get into the data:

- Non-farm payrolls increased by 254,000 jobs in September. The Labor Department’s Bureau of Labor Statistics report was well above consensus expectations. The unemployment rate dropped to 4.1%.

- Inflation as measured by CPI decreased further. CPI rose 2.5% for the 12 months ended in August, down significantly from the July reading of 2.9%

- Consumers and their savings are healthy. Consumer spending increased 0.2% in August, and the personal savings rate stood at 4.8%.

- The Fed was decisive on rate cuts. Rates were slashed by 50 basis points, with the current target rate now 4.75%-5.00%.

What Does the Data Add Up To?

As of October 4th, the CME Fed Watch tool is suggesting a target rate probability of 79.8% that the Fed will only cut rates by a further 50 basis points by the end of the year.

The extremely strong labor market reading from September has served to reassure economists and market participants that the economy is not nearing a recession. However, it likely puts an end to the hopes that rates will drop precipitously and quickly. Powell will continue to be cautious, and with wage gains also robust in September, he will likely keep inflation front and center in making future rate cut decisions.

Strong non-farm payrolls don’t tell the entire story. The JOLTS report, Job Openings and Labor Turnover Survey, reported that the labor market is close to stasis. Layoffs are still low at 1% in August, and workers quitting their jobs are at the slowest pace since 2015, which signals a lack of confidence in finding a better job.

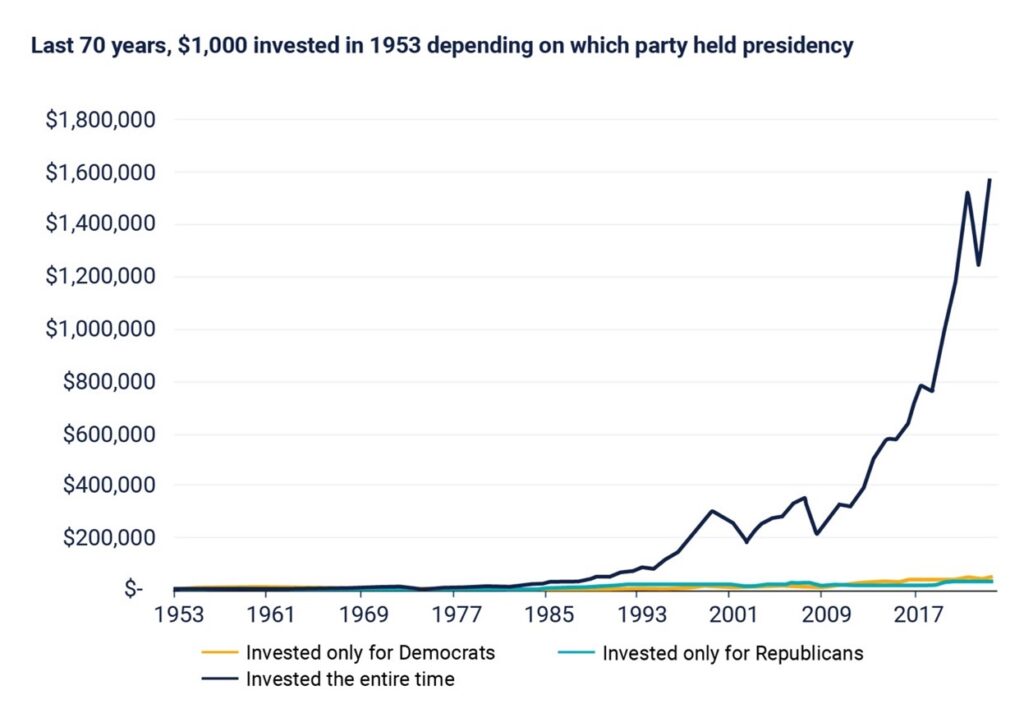

Chart of the Month: Do Elections Matter to Markets?

Elections bring uncertainty, and as the received wisdom goes, markets hate uncertainty. However, remaining invested regardless of the outcome is definitely the most advantageous idea.

Source: Blackrock and Morningstar, September 2024

Equity Markets in September

- The S&P 500 was up 2.02% for the month

- The Dow Jones Industrial Average rose 1.85%

- The S&P MidCap 400 was increased 0.98% for the month

- The S&P SmallCap 600 returned 0.67%

Source: S&P Global. All performance as of September 30, 2024

After declines in the first week of the month, eight of the eleven GICS sectors turned in positive performance. Consumer Discretionary did the best with a 7.02% return. Energy was the worst performer, with -2.78% return for the month. The Magnificent 7’s returned to dominance contributing 55.2% of September’s return.

Bond Markets in September

The 10-year U.S. Treasury ended the month at a yield of 3.78%, down from 3.91% the prior month. The 30-year U.S. Treasury ended September at 4.13%, down from 4.20%. The Bloomberg U.S. Aggregate Bond Index returned 1.34%. The Bloomberg Municipal Bond Index returned 0.99%.

The Smart Investor

Interest rates are falling, but they may not go as low or as fast as investors originally thought given Powell’s big lead off to the change in monetary policy. Investors holding cash may want to rethink that position as the uncertainty or interest rates and an election year gets resolved over the next few months.

Staying invested and staying on top of long-term goals is the most important principle in time of uncertainty. Focus on the financial planning that can contribute to your overall plan: maximizing tax efficient investments, using charitable donations wisely, and ensuring that your portfolio is keeping up with the changes in the economy and interest rates.

Combining personal goals, investments, and a view on the economy is at the core of what a financial advisor can bring to the table. We’re always here to help.

October Market Commentary – A Volatile Start to the End of the Year?

October Market Commentary – A Volatile Start to the End of the Year?

September Recap and October Outlook

September equity markets ended the month in positive territory, but with volatility increased. The VIX, the markets “fear index” closed higher than last month, at 16.73, up from 15.00. Intramonth, the values ranged from a high of 23.76 and a low of 14.90.

September’s somewhat surprisingly 50-basis point reduction in interest rates kicked of the regime change in monetary policy with a big move downwards. Subsequent data releases, including a particularly strong September non-farm payrolls number, may put a damper on expectations going forward, but the long-awaited loosening cycle is finally here. However, with an election looming and heightened tension in the middle east volatility will continue to affect markets and investor behavior alike.

Let’s get into the data:

What Does the Data Add Up To?

As of October 4th, the CME Fed Watch tool is suggesting a target rate probability of 79.8% that the Fed will only cut rates by a further 50 basis points by the end of the year.

The extremely strong labor market reading from September has served to reassure economists and market participants that the economy is not nearing a recession. However, it likely puts an end to the hopes that rates will drop precipitously and quickly. Powell will continue to be cautious, and with wage gains also robust in September, he will likely keep inflation front and center in making future rate cut decisions.

Strong non-farm payrolls don’t tell the entire story. The JOLTS report, Job Openings and Labor Turnover Survey, reported that the labor market is close to stasis. Layoffs are still low at 1% in August, and workers quitting their jobs are at the slowest pace since 2015, which signals a lack of confidence in finding a better job.

Chart of the Month: Do Elections Matter to Markets?

Elections bring uncertainty, and as the received wisdom goes, markets hate uncertainty. However, remaining invested regardless of the outcome is definitely the most advantageous idea.

Source: Blackrock and Morningstar, September 2024

Equity Markets in September

Source: S&P Global. All performance as of September 30, 2024

After declines in the first week of the month, eight of the eleven GICS sectors turned in positive performance. Consumer Discretionary did the best with a 7.02% return. Energy was the worst performer, with -2.78% return for the month. The Magnificent 7’s returned to dominance contributing 55.2% of September’s return.

Bond Markets in September

The 10-year U.S. Treasury ended the month at a yield of 3.78%, down from 3.91% the prior month. The 30-year U.S. Treasury ended September at 4.13%, down from 4.20%. The Bloomberg U.S. Aggregate Bond Index returned 1.34%. The Bloomberg Municipal Bond Index returned 0.99%.

The Smart Investor

Interest rates are falling, but they may not go as low or as fast as investors originally thought given Powell’s big lead off to the change in monetary policy. Investors holding cash may want to rethink that position as the uncertainty or interest rates and an election year gets resolved over the next few months.

Staying invested and staying on top of long-term goals is the most important principle in time of uncertainty. Focus on the financial planning that can contribute to your overall plan: maximizing tax efficient investments, using charitable donations wisely, and ensuring that your portfolio is keeping up with the changes in the economy and interest rates.

Combining personal goals, investments, and a view on the economy is at the core of what a financial advisor can bring to the table. We’re always here to help.

RECENT ARTICLES

Deferred Compensation – A Plan for Unlimited Retirement Savings

What a Weaker Dollar Means for Your Investments

June Market Commentary – The Limits of Data in an Ever-Changing Environment

Expanding Portfolio Horizons: Exploring Diversification Opportunities Beyond Major Indices

Understanding the Investment Implications of Rising Debt and Credit Downgrades